Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Earnings results often indicate what direction a company will take in the months ahead. With Q2 behind us, let’s have a look at Primoris and its peers.

Construction and maintenance services companies not only boast technical know-how in specialized areas but also may hold special licenses and permits. Those who work in more regulated areas can enjoy more predictable revenue streams - for example, fire escapes need to be inspected every five years. More recently, services to address energy efficiency and labor availability are also creating incremental demand. But like the broader industrials sector, construction and maintenance services companies are at the whim of economic cycles as external factors like interest rates can greatly impact the new construction that drives incremental demand for these companies’ offerings.

The 12 construction and maintenance services stocks we track reported a very strong Q2. As a group, revenues beat analysts’ consensus estimates by 4.4% while next quarter’s revenue guidance was in line.

Thankfully, share prices of the companies have been resilient as they are up 7.6% on average since the latest earnings results.

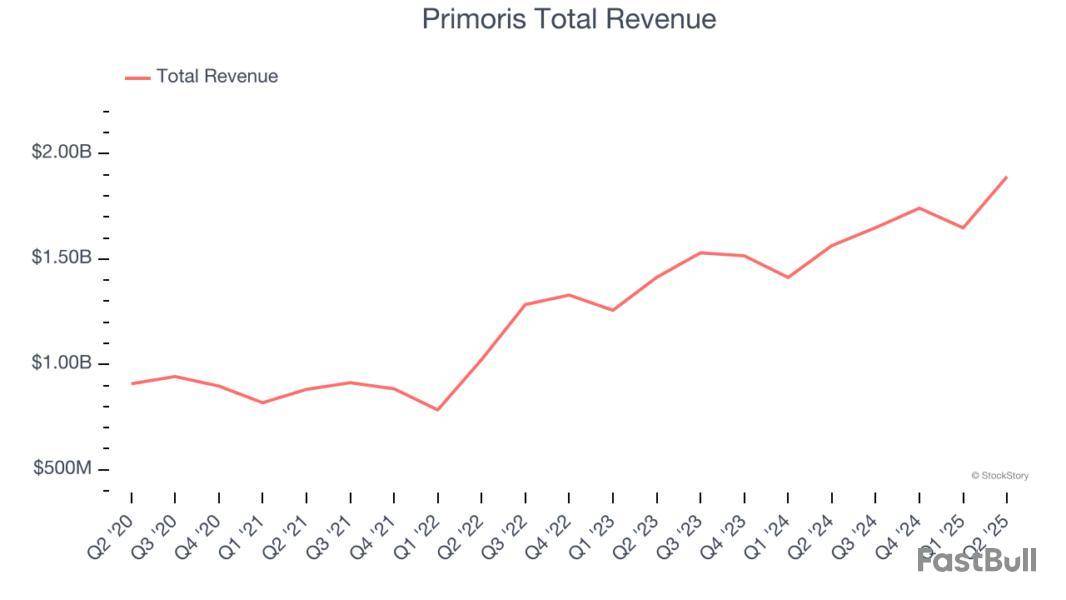

Listed on the NASDAQ in 2008, Primoris builds, maintains, and upgrades infrastructure in the utility, energy, and civil construction industries.

Primoris reported revenues of $1.89 billion, up 20.9% year on year. This print exceeded analysts’ expectations by 12.1%. Overall, it was an incredible quarter for the company with a beat of analysts’ EPS andEBITDA estimates.

Primoris pulled off the biggest analyst estimates beat of the whole group. Unsurprisingly, the stock is up 24.6% since reporting and currently trades at $116.12.

We think Primoris is a good business, but is it a buy today? Read our full report here, it’s free.

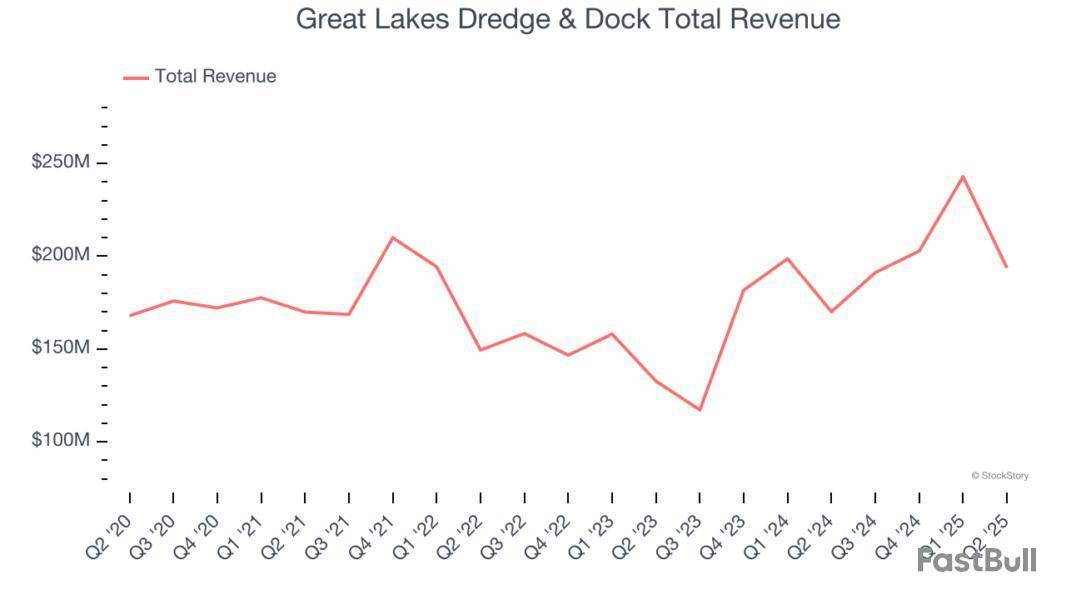

Founded as Lydon & Drews dredging company, Great Lakes Dredge & Dock provides dredging services, land reclamation, and coastal protection projects in the United States and internationally.

Great Lakes Dredge & Dock reported revenues of $193.8 million, up 13.9% year on year, outperforming analysts’ expectations by 9%. The business had an incredible quarter with a beat of analysts’ EPS and EBITDA estimates.

The market seems happy with the results as the stock is up 10.9% since reporting. It currently trades at $11.77.

Is now the time to buy Great Lakes Dredge & Dock? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: WillScot Mobile Mini

Originally focusing on mobile offices for construction sites, WillScot provides ready-to-use temporary spaces, largely for longer-term lease.

WillScot Mobile Mini reported revenues of $589.1 million, down 2.6% year on year, in line with analysts’ expectations. It was a softer quarter as it posted a significant miss of analysts’ adjusted operating income estimates and a significant miss of analysts’ EPS estimates.

WillScot Mobile Mini delivered the weakest full-year guidance update in the group. As expected, the stock is down 19.8% since the results and currently trades at $23.53.

Read our full analysis of WillScot Mobile Mini’s results here.

Founded in 2001, Construction Partners is a civil infrastructure company that builds and maintains roads, highways, and other infrastructure projects.

Construction Partners reported revenues of $779.3 million, up 50.5% year on year. This print lagged analysts' expectations by 1.3%. Aside from that, it was a mixed quarter as it also recorded full-year EBITDA guidance beating analysts’ expectations but a miss of analysts’ EPS estimates.

Construction Partners pulled off the fastest revenue growth among its peers. The stock is up 27.3% since reporting and currently trades at $119.09.

Read our full, actionable report on Construction Partners here, it’s free.

Having played a role in the construction of the Hoover Dam, Granite Construction is a provider of infrastructure solutions for roads, bridges, and other projects.

Granite Construction reported revenues of $1.13 billion, up 4% year on year. This number came in 3% below analysts' expectations. Taking a step back, it was still a strong quarter as it recorded full-year revenue guidance exceeding analysts’ expectations and an impressive beat of analysts’ EBITDA estimates.

Granite Construction had the weakest performance against analyst estimates among its peers. The stock is up 15.7% since reporting and currently trades at $108.10.

Read our full, actionable report on Granite Construction here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up