Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Exercising patience might be the most difficult part of investing. However, I find it much easier to patiently own some stocks more than others.

You might think that stocks with high dividend yields wouldn't be in that group. After all, such dividends can often be unsustainable. That isn't always the case, though. Here are five high-yield stocks I plan on holding for the next 10 years or longer.

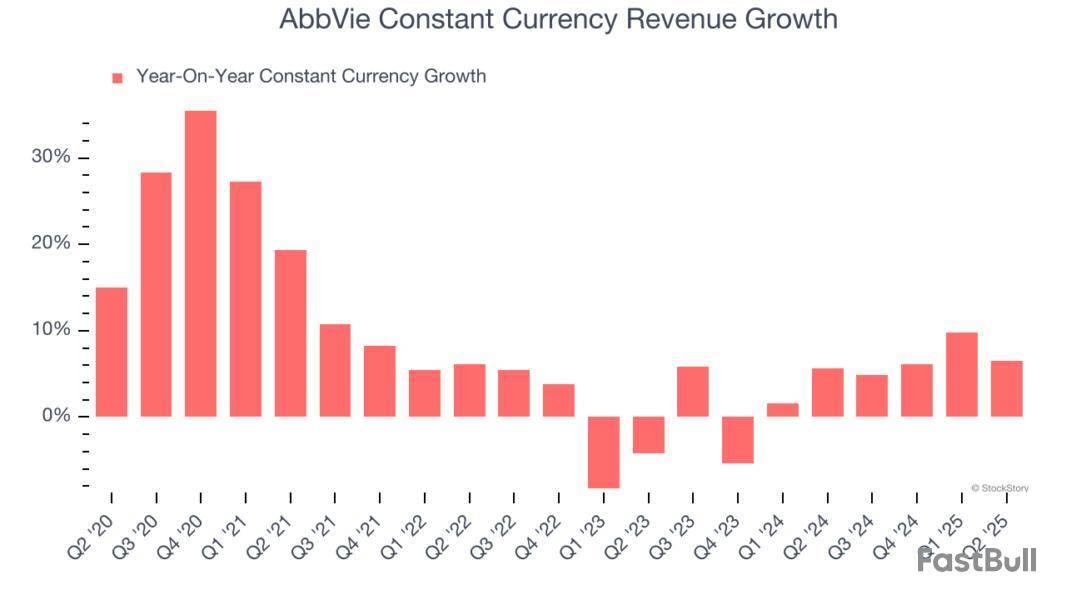

AbbVie (NYSE: ABBV) has proved that it's able to easily navigate one of the biggest challenges for a drugmaker: a patent cliff. The company's autoimmune-disease drug Humira once generated more than 60% of its total sales and ranked as the world's best-selling drug. But AbbVie hasn't skipped a beat since Humira lost U.S. patent exclusivity in 2023.

The company invested in research and development. It made smart acquisitions. Today, it's growing despite plunging sales for Humira. Although the big pharma company will face more patent expirations for other drugs in the future, I'm confident it will be able to survive and thrive over the long run.

I also have a warm and fuzzy feeling about the sustainability of AbbVie's dividend. The company is a Dividend King, with 53 consecutive years of dividend increases. Its payout has soared 310% since AbbVie was spun off from Abbott Labs in 2013 and now yields a healthy 3.16%.

Enbridge (NYSE: ENB) highlighted its "low-risk, utility-like business profile" to investors in its second-quarter update. That's the kind of business I can be comfortable owning part of for the next 10 years or longer.

By the way, Enbridge's management wasn't exaggerating. The company's pipelines transport 30% of all crude oil produced in North America and 20% of all natural gas consumed in the U.S. Enbridge is the largest natural gas utility in North America based on volume. It's investing in renewable energy. And the company projects roughly $50 billion in growth opportunities through the end of this decade.

Enbridge offers a forward dividend yield of 5.71%. While the stock isn't a Dividend King like AbbVie, the company has an impressive 30 consecutive years of dividend increases.

Enterprise Products Partners (NYSE: EPD) has a lot in common with Enbridge. It's also a midstream energy leader, with over 50,000 miles of pipeline spanning the U.S. that transport natural gas, natural gas liquids (NGLs), crude oil, and other refined products.

Two key differences between Enterprise Products Partners and Enbridge stand out. First, it doesn't run a natural gas utility, as Enbridge does. Second, Enterprise is a limited partnership (LP) rather than a corporation. LPs come with some tax hassles, but I think the advantages of owning Enterprise are worth the extra work.

Notably, Enterprise Products Partners pays an especially juicy distribution that yields 6.82%. The LP has also increased its distribution for 27 consecutive years.

Realty Income (NYSE: O) listed its shares on the New York Stock Exchange in 1994. Since then, the company has delivered a positive operational return (defined as the sum of annual adjusted funds from operations per share growth and dividend yield) every year.

I like that this real estate investment trust (REIT) has a highly diversified property portfolio, with 1,630 clients representing 91 industries. I like its triple-net-lease business model, which shifts most costs to tenants. I also like its growth opportunities, especially in Europe, where it faces only one major rival in a total addressable market of around $8.5 trillion.

And I love Realty Income's monthly dividend, which currently yields 5.55%. I also love that the company has increased its payout for 30 consecutive years.

Verizon Communications (NYSE: VZ) ranks as one of the world's largest wireless providers. The high costs associated with building out wireless networks present a formidable entry barrier for new competitors. Verizon already more than holds its own with current rivals, generating industry-leading wireless service revenue in its latest quarter.

Sure, this telecom stock's performance hasn't been great over the last five and 10 years. However, Verizon's business is humming along now. The company could also have a tremendous opportunity with 6G networks expected to roll out by the end of the decade.

I expect the dividend program will increase the chances that the stock delivers strong total returns. The dividend currently yields a mouthwatering 6.17%. Verizon has increased its dividend for 18 consecutive years, a streak that I think will soon be extended.

Before you buy stock in AbbVie, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and AbbVie wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $651,599!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,067,639!*

Now, it’s worth noting Stock Advisor’s total average return is 1,049% — a market-crushing outperformance compared to 185% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 25, 2025

Keith Speights has positions in AbbVie, Enbridge, Enterprise Products Partners, Realty Income, and Verizon Communications. The Motley Fool has positions in and recommends AbbVie, Abbott Laboratories, Enbridge, and Realty Income. The Motley Fool recommends Enterprise Products Partners and Verizon Communications. The Motley Fool has a disclosure policy.

5 High-Yield Dividend Stocks I Plan on Holding for the Next 10 Years or Longer was originally published by The Motley Fool

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up