- XAUUSD

- XAGUSD

- WTI

- USDX

Markets

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

Geopolitics may try to steal the limelight from US data.A possible US Supreme Court ruling on tariffs could dictate market movements.Dollar strength might be tested if investors refocus on Fed expectations.A crammed data calendar next week, US CPI comes on Tuesday; Fedspeak to intensify.Euro weakness persists, lingering risk of deterioration in US-EU relations.

At the tail end of 2025, most investors focused on Fed rate cut expectations and AI developments further reshaping the global economy. The nonexistent Santa Rally disappointed equity investors, but with most investment banks remaining quite optimistic about the 2026 performance, the mood could not be characterized as negative.

However, these expectations have been put aside, as US President Trump has other priorities. The transfer of Venezuelan President Maduro to the US to face heavy criminal charges and the control of Venezuela's vast oil reserves, with US firms ready to invest heavily in the aging infrastructure, have changed the market narrative.

With every win, Trump becomes bolder in his strategy. Following the Maduro operation, his focus quickly shifted to Colombia, Cuba and Greenland, bolstering the USA's foothold in the region after a period of relative inactivity. Greenland is the most intriguing case, as the US is trying to grab land from an ally and NATO member. Few expect this effort to fail, particularly as the US President has not excluded the military option to achieve his target.

Adding Iran to the mix, which was the main topic of discussion at the late-December meeting between Trump and Israel's Netanyahu, means then 2025, with its tariff shenanigans and the April market rout, might end up being a walk in the park for investors compared to 2026.

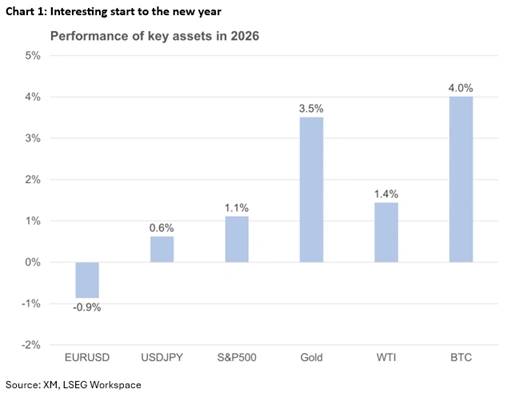

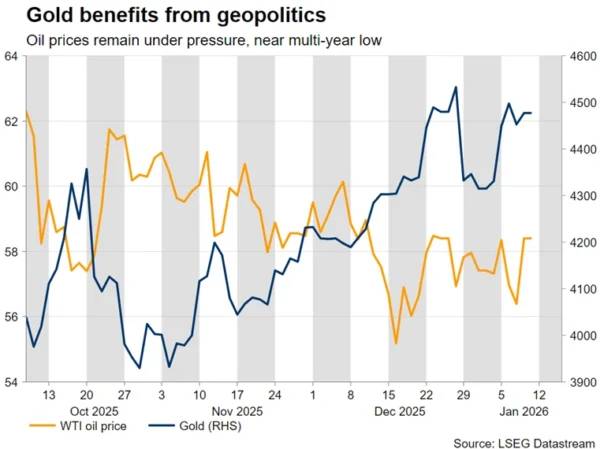

Both gold and oil have been quite responsive to the geopolitical developments, moving in opposite directions. Gold rallied towards the $4,500 level before correcting lower, partly dragged by silver's erratic behaviour, while oil has been drifting lower as the excess supply story for 2026 could get even worse if US firms gradually restore the flow of Venezuelan oil. Coupled with decent chances of a Ukraine-Russia ceasefire, the outlook remains bleak for the oil market, with the five-year low of $55.19 around the corner.

Notably, Secretary of State Rubio is scheduled to visit Denmark next week, carrying Trump's Greenland offer to Denmark, while the US President is expected to maintain his bold rhetoric on this issue. Gold stands ready to benefit from a likely deterioration of the EU-US relations and the previously unthinkable threat of military use in Greenland.

Amidst this volatile environment, there is growing speculation that on Friday, January 9, the US Supreme Court might announce its ruling on the legality of tariffs, after 10 am EST (3 pm GMT).

Should the ruling be positive, essentially confirming Trump's ability to impose tariffs without Congress's consent, Trump could restart his tariff rhetoric, targeting China and particularly Europe. He might feel compelled to threaten the EU with aggressive tariffs as a means to "acquire" Greenland.

If the ruling is negative, branding tariffs imposed using a 1977 law as illegal, Trump's reaction could prompt an acute market reaction, although his administration has already drawn up a plan B to reimpose the existing tariffs under different legislation.

Gold stands ready to benefit under both aforementioned scenarios, particularly if the ruling deems current tariffs illegal. On the flip side, investors tend to shun the dollar during trade flare-ups, boosting other currencies like the euro and the Swiss franc.

What would be extremely interesting is if the Supreme Court sets boundaries to the President's power, essentially limiting his ability to authorize tariffs or greenlight military operations without approval from Congress. Such a development could make Trump even more unpredictable going forward.

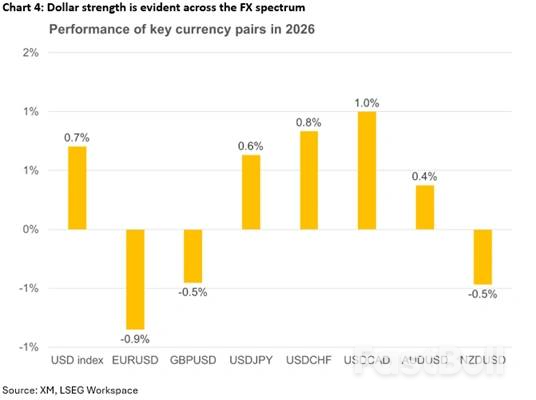

The US dollar has started the new year on the right foot, outperforming both the euro and the pound, as developments regarding Venezuela have prompted an odd risk-off reaction in markets, with US equities also faring relatively well. The pound performance has been a surprise, with the focus now shifting to Thursday's monthly GDP print for November.

On the other hand, the lack of new bullish catalysts is contributing to the euro's current weakness. More importantly, considering Rubio's visit to Denmark, the euro's appeal might be dented by the possibility of an aggressive deterioration in US-EU relations, damaging the momentum built in the Eurozone economy due to the much-discussed aggressive fiscal spending. The ECB remains on the sidelines, but a severe economic downturn, mostly driven by a protracted trade flare-up, might be forced to reassess its current balanced policy stance.

Putting geopolitics aside, a return to normal newsflow might dent the dollar's current appeal, as investors refocus on Fed rate cut expectations.

Stronger data releases, like Wednesday's impressive ISM Services PMI survey, might keep the dollar bid, but investors are still convinced that the one rate cut pencilled in by policymakers in the December 2025 dot plot is too cautious. On the flip side, with around 60bps of easing currently priced in for 2026, investors are currently more comfortable with weaker data prints and appear ready to sell the dollar.

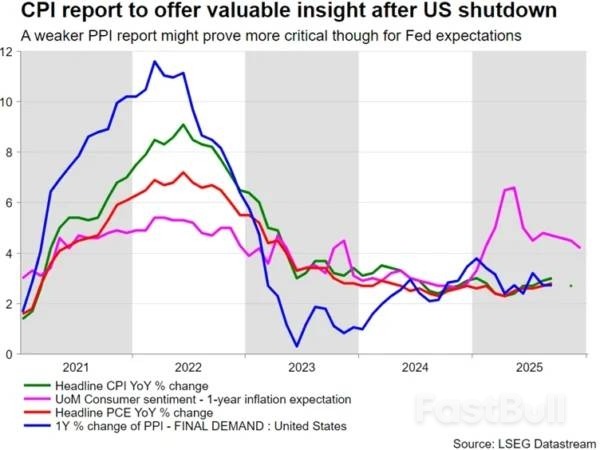

Next week, the calendar is crammed with pivotal data, mostly focusing on inflation and the consumer side of the US economy. On Tuesday, the December CPI report will be in the spotlight, the first inflation print potentially not affected by the US government shutdown.

Another deceleration in price pressures, partly contradicting Fed members' expectations for near-term inflation to remain elevated, as seen in the December 10 Fed meeting minutes, would potentially play into the hands of the new Fed Chair, potentially bringing forward the first 25bps rate cut currently priced in for mid-June. Notably, Trump has been mum on the name of Powell's replacement.

On Wednesday, retail sales and producer price index data for November will be released, with the former giving significant insight into consumer spending appetite. A strong set of figures could beef up the current 2.7% growth forecast by the Atlanta Fed GDPNow model.

Meanwhile, after a relatively quiet period, Fedspeak is expected to intensify. The next Fed meeting is just 20 days away, which means that Fed members have to put their arguments across ahead of the usual blackout period. The focus will be on the more hawkish voting members, like Cleveland's Hammack and Dallas' Logan. Interestingly, the doves clearly have the upper hand this year in terms of the votes, adding to expectations for a persistently dovish Fed stance in 2026.

It has been a difficult start to the new year for peripheral currencies. Central bank rate expectations should be at the forefront, but, for now, dollar strength is dominating the moves. Apart from the Aussie, which is marginally gaining against the greenback, the remaining currencies are on the back foot at this stage versus the dollar, despite their respective central banks completing their easing cycles.

Specifically, developments with Venezuela could turn into a serious headache for Canada. A good part of Canada's production is heavy oil, which is also the dominant product of Venezuela, further denting PM Carney's bargaining power with President Trump, who is not the biggest fan of Canada.

Similarly, Australia is closely monitoring China's newsflow. There is a renewed attempt by Chinese authorities to improve the situation on the ground by expediting investment plans and further allowing banks to address bad loans, in order to beef up their financial health and profitability. Notably, on Wednesday, Chinese trade balance data for December will be published, with investor attention on whether exports maintain their recent robust annual pace of increase and imports continue to grow, validating China's efforts to prop up domestic demand.

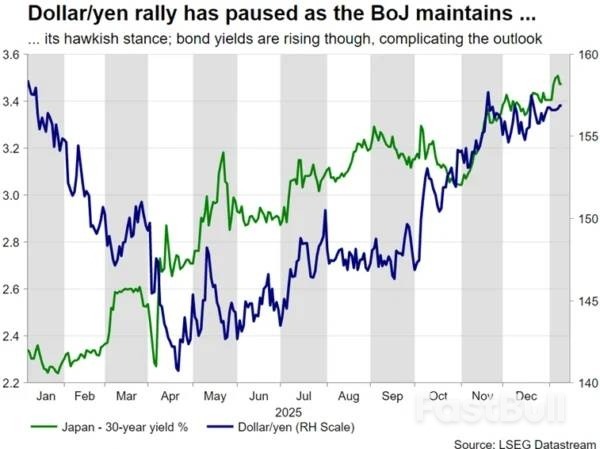

Finally, the yen has been resisting the dollar's strength, courtesy of the hawkish BoJ. Investors are trying to bring forward the next rate hike, currently priced in for September, but mixed data have been muddling the outlook. The BoJ will probably have to wait until the Shunto round, which realistically means that the April meeting is the key one for the next move. Until then, Japanese government officials will probably continue to verbally intervene to keep dollar/yen well below the ¥160, unless of course, the Fed surprises with a Q1 rate cut.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

Log In

Sign Up