Some currencies have stood up to a market storm

The Russian economy will grow by 0.8% this year, down from a forecast of 1% a month ago, according to a Reuters poll, echoing an earlier government announcement that the official forecast could be downgraded.

The turmoil in the Middle East not only alleviates some fiscal pressures but also serves as a distraction from problems that have dogged Russia’s economy, particularly persistently high inflation.

Federal budget deficit surged past full-year target in Q1, underscored by a sharp decline in energy tax receipts and a double-digit spike in government spending, according to Finance Ministry data.

Hungarian voters delivered a shock election result on Sunday, ending Viktor Orban’s 16-year rule. The new pro-EU government led by Peter Magyar will pose another challenge to Putin.

Orban was one of the few leaders within Europe to maintain close ties to Moscow. Not only did he refuse to cut down on Russian energy imports, but thwart the efforts to support Kyiv by veto.

Russia has been helping Iran to target US bases in the Middle East, said Zelenskyy. Whether the claim holds water, further declines in the OPEC’s crude output would somewhat counterbalance the ongoing sanctions.

The country’s strategic pivot eastward leaves China in a better position to navigate the emerging supply crunch. The yuan’s downside is thus likely limited, with potentially solid support at 0.8 per dollar.

Oil windfall

Europe boosted imports from Russia’s flagship LNG project in the first three months of the year, as supplies of Qatari LNG have dried up following damage to the energy infrastructure.

Russia holds the world's largest natural gas reserves. Still more than two-thirds of the LNG imported to the bloc to date has come from the US, according to the European Commission data.

European average gas storage levels remain below normal averages ahead of the key summer refilling season. That primes Norway, which is the only major producer in the region, for aggressive capacity expansion.

Norway supplies nearly a third of Europe's gas needs. The country’s energy executives hope that the fresh anxiety about energy supply will lead the EU to rethink its moratorium on Arctic drilling.

The moratoriums in place are primarily driven by the need to protect fragile ecosystems, prevent catastrophic oil spills in icy, unmanageable conditions, and combat climate change.

The positive terms-of-trade shock sent the Norwegian Krone higher by roughly 6% year to date. The country’s combined oil and gas production exceeded an official forecast by 1.1% in March.

Norges Bank left interest rates unchanged at its March meeting, suggesting a tighter monetary policy later this year. Inflation jumped to 3.6% in March, which could help hasten the process.

One-sided race

The Swiss franc is currently trading above the key 200 level against the yen again, within an inch of its record peak hit last month. That underscores the continual divergence between the currencies.

Switzerland’s inflation rate jumped in March to the quickest pace in a year, but the increase of 0.3% fell well short of the 0.5% estimate. Higher energy prices were mostly offset by a stronger franc.

Even with the jump in March, the European country on the verge pf deflation appears to be confronting few price pressures. For all of 2026, the SNB expects it to average 0.5%.

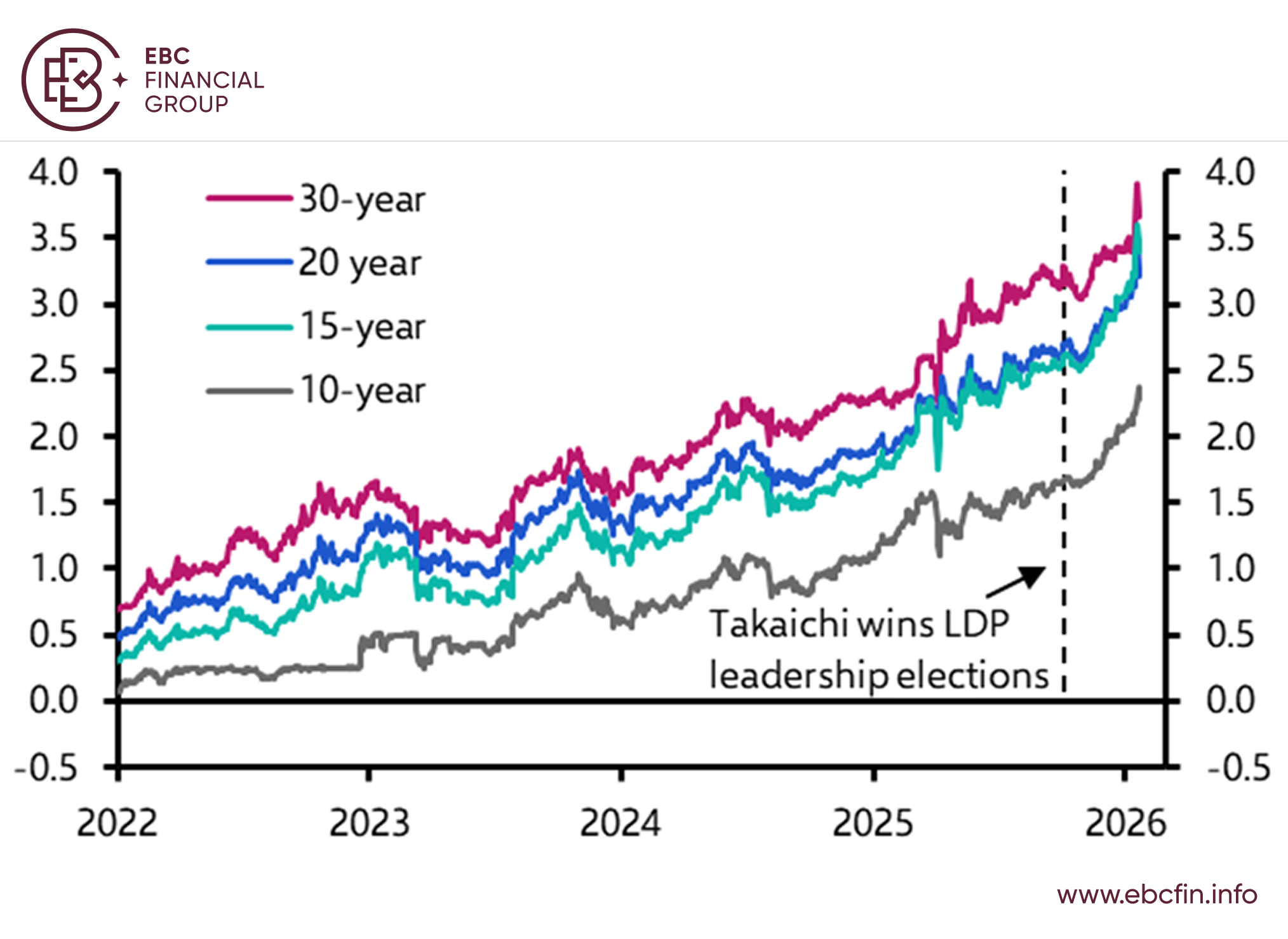

Japan’s inflation is projected to grow 1.8% from a year earlier last month. Long-term government bond yields hit a 29-year high of 2.49% on Monday, as rising import costs will worsen the enormous debt burden.

Recent surveys showed business and household sentiment worsened sharply. The BOJ is expected to cut growth forecasts and revise up inflation projections in a quarterly report.

Mitsubishi UFJ Morgan Stanley Securities analyst said "keeping rates steady (in April) could also push up yields and weaken the yen on fear the BOJ is behind the curve in addressing inflation."

Given the yen above 160 per dollar, Tokyo may prefer steering away from forex intervention before more clarity on the market direction. The Swiss franc still have the upper hand at least in the short term.

Disclaimer: This material is for general information purposes only and is not intended as (and should not be considered to be) financial, investment or other advice on which reliance should be placed. No opinion given in the material constitutes a recommendation by EBC or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person.

Copyright © 2026 FastBull Ltd

风险提示

外汇交易具有很高的风险,可能并不适合所有投资者。杠杆可能会造成额外的损失风险。在决定参与外汇交易商之前,请仔细考虑您的投资目标、经验水平和风险承受能力。您可能会损失部分或全部初始投资,真诚的建议您,不要投资承受不起的风险交易。请经常提醒自己参与外汇交易的风险,如果有任何疑问,请咨询独立的财务或税务顾问。我们提供的任何数据和信息,均来自交易商和各国外汇监管机构的官方数据,仅出于提供信息的目的,不作为交易建议。另外,过去的表现并不预示未来的结果。

免责声明

本网站所含数据未必实时、准确。本网站的数据和价格未必由市场或交易所提供,而可能由做市商提供,所以价格可能并不准确且可能与实际市场价格行情存在差异。即该价格仅为指示性价格,反映行情走势,不宜为交易目的使用。对于您因交易行为或依赖本网站所含信息所导致的任何损失,本网站所含数据的提供商不承担责任。