From $6 to $120+: Has Palantir Peaked — or Is There More Upside?

Palantir is no longer a hidden AI stock. After climbing from around $6 in late 2022 to more than $120, the company has become one of the biggest winners of the AI boom. The key question for investors is no longer whether Palantir can grow, but whether enough future growth remains to justify today's valuation.

This debate sits at the center of nearly every Palantir stock 2030 price prediction. Bulls argue that the company is still in the early stages of monetizing enterprise AI, while bears believe much of that opportunity has already been priced in.

Up 1,000% in Two Years — What Does the Valuation Actually Say?

A 1,000% gain naturally raises concerns about whether investors are arriving too late. However, stock performance alone does not determine whether a company is overvalued. What matters is how fast the underlying business can continue growing.

Palantir's recent rally has been supported by strong commercial revenue growth, accelerating AI Platform (AIP) adoption, and expanding profitability. Revenue has grown far faster than many investors expected just a few years ago.

Still, valuation remains the biggest challenge. When a company reaches a market capitalization of hundreds of billions of dollars, future returns become increasingly dependent on execution rather than sentiment.

| Question | What Matters Most? |

|---|---|

| Can revenue keep growing above 30%? | Supports premium valuation |

| Can AI demand remain strong? | Drives customer expansion |

| Can margins continue improving? | Supports higher earnings power |

| Can valuation stay elevated? | Critical for future share-price gains |

In other words, the next phase of returns will likely depend more on business execution than multiple expansion.

P/S Above 100x — Which Companies Have Survived This?

One reason Palantir attracts criticism is its historically extreme price-to-sales ratio. At various points during its rally, investors valued the company at more than 100 times annual revenue.

History shows that very few companies have successfully grown into such valuations. The ones that did generally shared three characteristics:

- Large and expanding addressable markets

- Sustained revenue growth above industry averages

- Strong competitive advantages that limited pricing pressure

Examples often cited include Nvidia, Amazon during its early expansion years, and Salesforce during the early cloud-computing cycle. These companies eventually justified lofty valuations by dramatically increasing revenue and profitability over time.

The challenge for Palantir is that maintaining a premium valuation becomes harder as the company grows larger. Investors do not need perfection, but they do need evidence that AI-driven growth can continue for many years.

Buying the Top vs. Missing the Next Rally — Where Investors Stand

Today's Palantir debate is remarkably similar to what investors faced with other transformative technology companies in the past. Buying after a 1,000% rally feels risky. Yet waiting for a major correction can also mean missing another leg higher if growth continues exceeding expectations.

| Bull Case | Bear Case |

|---|---|

| Enterprise AI adoption is still in its early innings | Most AI optimism is already reflected in the stock |

| AIP becomes a core operating layer for large organizations | Competition limits long-term pricing power |

| Revenue growth remains above 30% for years | Growth slows as the business matures |

| Premium valuation remains justified | Valuation compresses despite business growth |

Ultimately, investors are not debating Palantir's quality. They are debating how much future growth is already reflected in the stock price. That distinction is important because even exceptional companies can generate disappointing returns if expectations become too aggressive.

This is why any serious Palantir 2030 stock price prediction must focus on future revenue growth, valuation multiples, and AI adoption trends rather than past share-price performance alone.

How Much Upside by 2030? Three Scenarios

Most Palantir stock price predictions fail because they focus on a single target price. In reality, PLTR's future value depends on a range of outcomes driven by revenue growth, valuation multiples, and execution. Rather than guessing one number, investors should think in probabilities.

| Scenario | 2030 Share Price | Revenue Growth | Valuation | Probability |

|---|---|---|---|---|

| Bear Case | $140 | Growth slows significantly | Major multiple compression | Possible |

| Base Case | $300 | Strong but sustainable growth | Premium valuation maintained | Most realistic |

| Bull Case | $700 | AI adoption accelerates | Exceptional valuation persists | Requires near-perfect execution |

$140 Bear Case — Limited Upside if Valuation Compresses

A $140 share price may sound optimistic compared with where Palantir traded just a few years ago, but it would represent a disappointing outcome for investors buying at current levels.

In this scenario, Palantir remains a successful company, but growth slows faster than the market expects. Commercial AI adoption becomes more gradual, government contracts grow at a moderate pace, and investors begin valuing the company more like a mature software business rather than a high-growth AI leader.

- Revenue growth falls toward the mid-teens

- Enterprise AI spending grows slower than expected

- Valuation multiples compress significantly

- Competitive pressure increases

The key lesson is that great businesses do not always generate great stock returns. If growth slows enough, valuation compression can offset years of revenue expansion.

$300 Base Case — About 130% Upside From a $130 Entry

The base case assumes Palantir continues executing well without completely dominating the AI software market. This is the scenario many long-term investors consider the most realistic.

- Revenue growth remains above industry averages

- Commercial customer count expands steadily

- AI adoption continues across large organizations

- Premium software valuation remains justified

A move to approximately $300 would still represent a strong long-term outcome. For investors using a $130 reference price, that would imply about 130% total upside and an annualized return near 18% to 20%, depending on the exact holding period.

$700 Bull Case — 4–5x, But Three Things Must Go Right

The $700 scenario is where Palantir transitions from a successful software company into one of the dominant AI infrastructure platforms in the world. For PLTR to approach $700 by 2030, three things likely need to happen:

- Revenue growth remains exceptionally high for most of the decade.

- AIP becomes deeply embedded within enterprise workflows across industries.

- Investors continue assigning Palantir a premium valuation relative to traditional software companies.

Supporters of this view argue that Palantir could become the operating system for enterprise AI, similar to how major cloud platforms became foundational infrastructure over the last decade. If that happens, today's valuation may ultimately look conservative.

Three Numbers That Could Decide Palantir's 2030 Price

Palantir's 2030 stock price will not be decided by AI hype alone. The real math comes down to three variables: how fast revenue grows, what sales multiple investors are willing to pay, and how much shareholder dilution occurs along the way.

| Scenario | 2030 Revenue | 2030 P/S Multiple | 2030 Diluted Shares | Implied 2030 Stock Price |

|---|---|---|---|---|

| Bear Case | $18.9B | 20x | 2.70B | About $140 |

| Base Case | $32.4B | 25x | 2.70B | About $300 |

| Bull Case | $37.8B | 50x | 2.70B | About $700 |

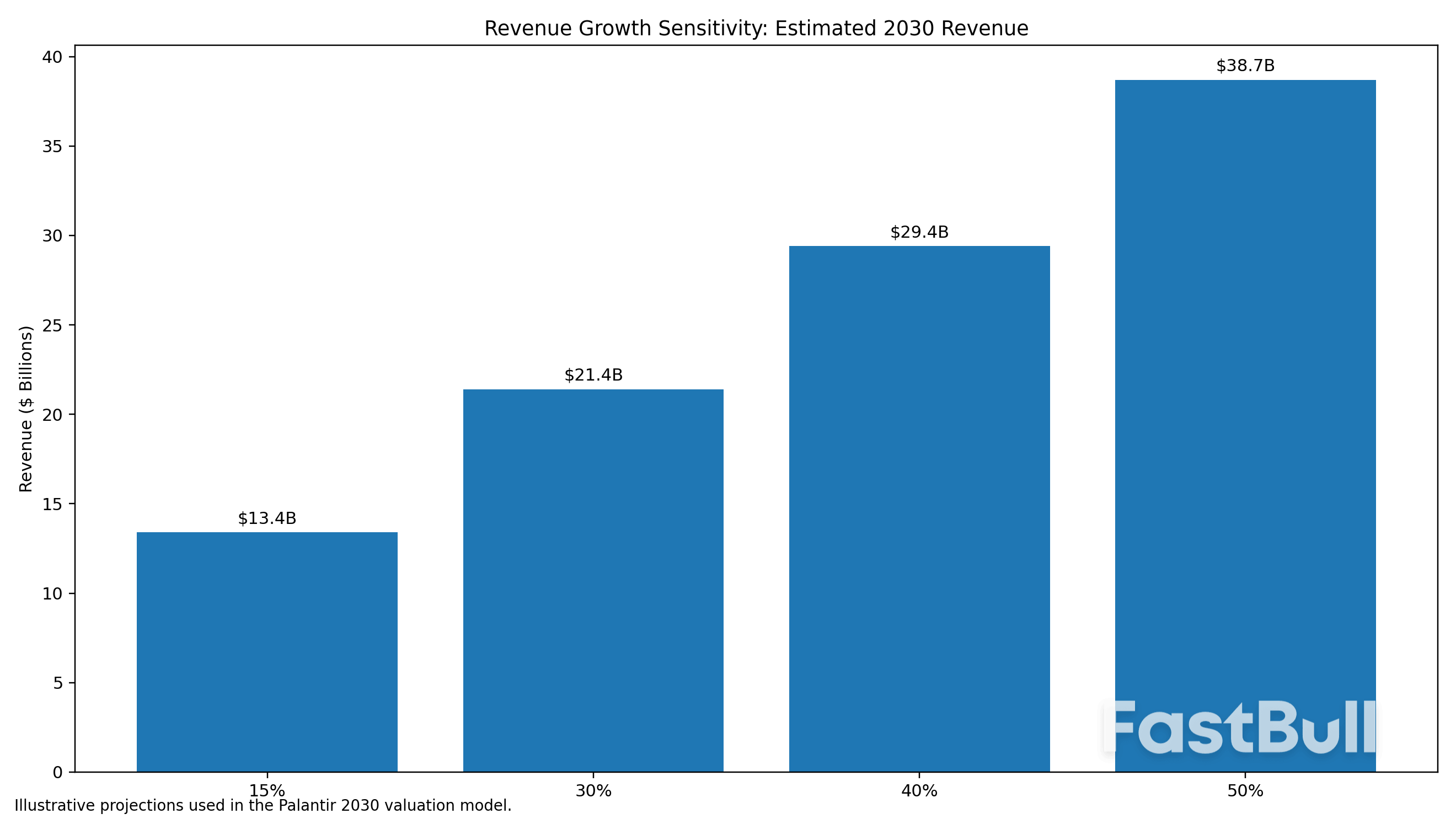

30% vs. 50% Revenue Growth — The Gap Between $300 and $700

Revenue growth is the most important number in the Palantir model. The table below is a sensitivity test, not a direct match to the bear, base, and bull cases above. From a 2026 revenue base of about $7.65 billion, Palantir would reach roughly $21.4 billion in 2030 revenue at a 30% CAGR and about $38.7 billion at a 50% CAGR.

| Revenue CAGR 2026–2030 | Estimated 2030 Revenue | What It Would Mean for PLTR |

|---|---|---|

| 15% | About $13.4B | Growth slows sharply; hard to justify a premium AI valuation |

| 30% | About $21.4B | Strong growth, but likely not enough by itself to support $700 |

| 40% | About $29.4B | Enough to make a $300 target more realistic if valuation remains high |

| 50% | About $38.7B | Needed for the bull case, but difficult to sustain at scale |

This is why AI adoption matters so much. Palantir does not need AIP to be a popular software product; it needs AIP to become a mission-critical operating layer for large enterprises and government agencies.

Can the Sales Multiple Hold? Why $700 Needs More Than a 20x P/S

The sales multiple is the second number investors cannot ignore. Palantir currently trades at an extremely high sales multiple because the market is pricing it as an AI infrastructure winner, not as a normal enterprise software company.

| 2030 Revenue | 8x P/S | 12x P/S | 20x P/S | 25x P/S | 50x P/S |

|---|---|---|---|---|---|

| $18.9B | $56 | $84 | $140 | $175 | $350 |

| $32.4B | $96 | $144 | $240 | $300 | $600 |

| $37.8B | $112 | $168 | $280 | $350 | $700 |

This table explains why a $700 target is possible but not easy. To reach that level, Palantir would likely need both exceptional revenue growth and an unusually high valuation multiple near 50x sales — a demanding combination that means investors would still need to believe in 2030 that Palantir deserves to trade more like an AI infrastructure platform than a traditional software company.

SBC, Government Contracts, and Global Expansion — Three Variables Most Forecasts Ignore

Most Palantir stock 2030 price prediction models focus only on revenue, but three overlooked variables can materially change the final share price:

- Stock-based compensation can dilute shareholders if employee equity grants continue to expand the share count.

- Government contracts can support durable revenue, but they also expose Palantir to budget cycles, procurement delays, and political risk.

- Global expansion can widen the revenue base, but international adoption may be slower due to data-sovereignty concerns and local competition.

| Variable | Why It Matters | Impact on 2030 Price |

|---|---|---|

| SBC and dilution | Changes the denominator in the valuation formula | Higher dilution lowers per-share upside |

| Government contracts | Supports revenue durability and national-security credibility | Stable contracts support the bear and base cases |

| Global expansion | Determines whether Palantir can scale beyond U.S.-led demand | Successful expansion helps justify the bull case |

The bottom line is that Palantir does not need everything to go right to reach $300. But it likely needs nearly everything to go right to reach $700: sustained AI-driven revenue growth, a premium sales multiple, limited dilution, durable government demand, and stronger global commercial adoption.

Is Palantir's Moat Real? An Honest Look at the Competition

Palantir's moat is real, but it is not invincible. The company has a rare combination of government credibility, operational AI software, security clearances, and enterprise deployment experience. However, by 2030, Palantir will still need to compete against larger cloud platforms, data infrastructure companies, and specialized enterprise AI vendors.

Classified Data Access — The Advantage Nobody Else Can Buy

Palantir's strongest competitive advantage comes from the environments where its software has already been deployed. The company is not simply selling dashboards or generic AI tools. It has spent years building software for defense, intelligence, public-sector, and other mission-critical use cases where trust, security, and operational reliability matter as much as product features.

| Moat Factor | Why It Matters | How Easy Is It to Replicate? |

|---|---|---|

| Government relationships | Supports long-cycle defense and public-sector contracts | Difficult |

| Security-sensitive deployments | Builds credibility in classified and mission-critical environments | Difficult |

| Ontology-based operating layer | Connects AI models to real business workflows and decisions | Moderate to difficult |

| AIP implementation process | Helps customers move from AI demo to operational use case | Moderate |

The most important point is that Palantir's moat is not just technical. It is institutional. Still, investors should avoid overstating this advantage — Microsoft, Google, Amazon, Snowflake, and other enterprise technology providers also have deep security capabilities and government relationships.

Palantir vs. Snowflake vs. C3.ai — Who Wins by 2030?

| Company | Core Strength | AI Positioning | Main Risk by 2030 |

|---|---|---|---|

| Palantir | Operational software for complex organizations | AIP connects AI to real-world workflows, decisions, and enterprise data | High valuation requires sustained growth and premium pricing power |

| Snowflake | Cloud data platform and governed enterprise data layer | Cortex AI helps customers build AI apps and insights inside Snowflake's data environment | May be viewed more as infrastructure than a high-margin AI application layer |

| C3.ai | Enterprise AI applications and industry-specific AI software | Offers AI platforms and applications for large organizations | Needs stronger growth, profitability, and market confidence to match larger rivals |

A more realistic 2030 outcome is that Snowflake owns more of the data layer, Microsoft and Google own more of the productivity and cloud AI layer, and Palantir wins in high-complexity operational AI use cases.

AIP Adoption vs. Microsoft and Google — Who Has the Edge?

| Platform | Primary Advantage | Where It Could Beat Palantir | Where Palantir Still Has an Edge |

|---|---|---|---|

| Microsoft | Enterprise distribution through Microsoft 365, Azure, Teams, and Copilot | Knowledge-worker productivity, low-friction AI adoption, broad enterprise access | Complex operational workflows that require deep customization and mission-critical deployment |

| Advanced AI models, cloud infrastructure, search, and data tools | AI agents, developer workflows, cloud-native AI applications, multimodal AI | Defense-grade operating environments and highly specialized operational AI implementation | |

| Palantir | Operational AI software built around enterprise ontology and deployment support | High-complexity AI use cases where generic tools are not enough | May lack the same distribution scale as hyperscale cloud platforms |

Microsoft and Google have a distribution advantage. Palantir has an implementation advantage. For simple enterprise AI use cases, Microsoft or Google may be the easier choice. For more complex use cases — a manufacturer optimizing production lines, a defense agency coordinating battlefield intelligence — Palantir's position is stronger.

The honest conclusion is that Palantir has a real moat, but its 2030 upside depends on whether that moat expands from government and high-complexity enterprises into a much broader commercial AI market.

Is PLTR Worth Buying Now?

PLTR may be worth buying now only for investors who believe Palantir can keep converting AI demand into exceptional revenue growth. At current valuation levels, the stock is not priced for average execution. It is priced for Palantir to remain one of the most important enterprise AI platforms through 2030.

| Investor Type | PLTR May Make Sense If... | PLTR May Be Too Risky If... |

|---|---|---|

| Long-term growth investor | You believe AIP can drive years of high commercial revenue growth | You need valuation support from current earnings or cash flow |

| AI-focused investor | You see Palantir as a core operating layer for enterprise AI | You believe Microsoft, Google, or Snowflake will absorb most AI demand |

| Risk-sensitive investor | You can tolerate major volatility and valuation compression | You cannot accept a scenario where the stock stays flat for years |

What Signals Confirm the Bull Case — and What Signals Mean Exit?

| Signal to Watch | Confirms the Bull Case If... | Warning Sign If... |

|---|---|---|

| Commercial revenue growth | Growth remains above 30% for several years | Growth falls toward the mid-teens |

| AIP adoption | More customers expand from pilots to full production deployments | AIP demand stays concentrated in limited use cases |

| Net dollar retention | Existing customers keep spending more over time | Expansion slows or large customers reduce commitments |

| Operating margins | Margins improve while revenue keeps growing quickly | Growth requires heavier sales spending or lower pricing |

| Stock-based compensation | Dilution remains controlled | Share count keeps rising faster than investors expect |

- A bullish signal: revenue growth staying above 30% while margins continue expanding.

- A neutral signal: solid growth, but with valuation slowly compressing toward mature software levels.

- A bearish signal: slowing growth combined with higher dilution and weaker customer expansion.

Base Case $300 — What's the Annualized Return From Here?

| Target Price by 2030 | Approximate Total Return From $130 | Approximate Annualized Return | What It Implies |

|---|---|---|---|

| $140 | About 8% | About 2% per year | Business grows, but valuation compresses heavily |

| $300 | About 130% | About 20% per year | Growth remains exceptional and valuation stays premium |

| $700 | About 438% | About 45% per year | Palantir becomes one of the dominant enterprise AI platforms |

The most balanced conclusion is that PLTR remains a high-upside but high-expectation stock. It may still reward long-term investors if AI adoption keeps accelerating, but the downside risk is meaningful if valuation compresses before revenue catches up.

FAQs

Final Verdict

This Palantir Stock Price Prediction 2030 comes down to one core question: can PLTR keep turning AI adoption into exceptional revenue growth? A $140 outcome suggests valuation compression wins, $300 requires strong execution, and $700 needs near-perfect AI monetization. Palantir remains a powerful company, but at today's price, investors are paying for extraordinary results.