Trader Exposes Ultima Markets Regulatory Arbitrage via Identical Entities and the $2,000 Settlement Cover-up

Not too long ago, a trader from Indonesia sought help from BrokersView, stating he was unable to withdraw approximately $1,455.71 from his Ultima Markets account. More recently in January, another trader from Germany revealed a hidden industry "rule" involving Ultima Markets at the painful cost of €14,522: when you think you are protected by regulation, you might have just fallen into a meticulously designed "identical clone" trap.

This complaint involving the broker Ultima Markets not only exposes the hidden nature of regulatory arbitrage but also tears away the mask of offshore licenses, revealing their powerlessness in actual dispute resolution.

"Ultima Markets Ltd" Is Not Equal to "Ultima Markets Ltd"

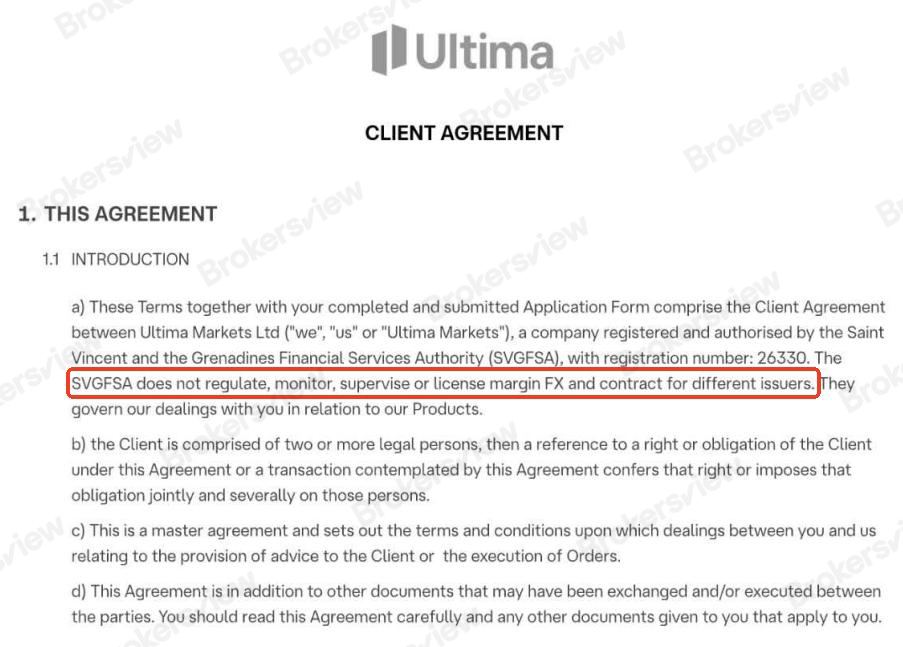

The core of this incident lies in the broker's name. When signing up, the trader was convinced they were opening an account under an entity regulated by the Financial Services Commission (FSC) of Mauritius, as the license number GB 23201593 was prominently displayed on the website. However, it was not until July 2025, when a dispute arose, that he discovered he had been silently transferred to an unregulated shell company in St. Vincent and the Grenadines (SVG).

The Mauritius-licensed entity and the unregulated company registered only in SVG use the exact same registered name—"Ultima Markets Ltd." This tactic of using identical entities for "internal cloning" makes it impossible for traders to detect that the legal counterparty has been swapped during the contract signing. It wasn't until the trader unearthed a hidden "Client Agreement" deep within the server that he saw the disclaimer in Clause 1.1(a): "The SVGFSA does not regulate, monitor, supervise or license margin FX."

Ineffective Regulation

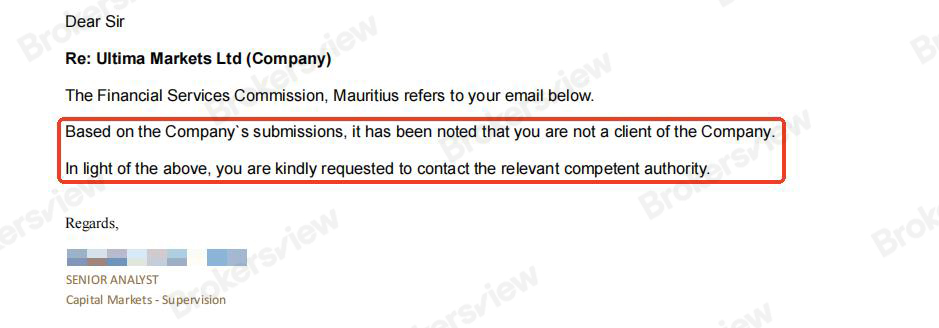

When the trader sought help from the FSC Mauritius, the regulator's response was disappointing. Although the FSC initially opened an investigation, it ultimately closed the case on the grounds of "no jurisdiction." The reasoning was simple: since a St. Vincent clause was hidden in the contract, from a legal perspective, this German investor was never a client of the FSC-licensed entity. This outcome proves that for users transferred to offshore entities via "bait and switch" tactics, the so-called regulatory license is nothing more than a scrap of paper.

Meanwhile, traditional financial institutions seem to have a sharper sense of risk than regulators. The victim's German bank (C24) has permanently blocked this broker and flagged it for "High Fraud Risk."

The $2,000 "Hush Money"

Faced with the allegations, Ultima Markets did not choose to fix its compliance loopholes but instead tried to resolve the person raising the issue with money. The broker offered the trader a $2,000 settlement on the condition that he delete negative reviews and withdraw the complaint filed with the regulator. Compared to the victim's loss of over €14,000, this amount appears to be "hush money" in a desperate attempt to cover up the truth.

As pointed out in online comments, this is not a simple dispute over trading losses, but a textbook case of regulatory arbitrage. The broker uses the brand equity of a licensed entity to acquire customers at the front end, while funneling them through a "secret channel" to an unregulated offshore black hole at the back end. In this process, all compliance reviews, risk disclosures, and informed consent mechanisms fail entirely.

BrokersView Reminds You

When signing a contract with a broker, do not just look at the brand name; carefully compare the specific legal entity mentioned in the client agreement. If a broker uses the exact same name across different jurisdictions, it is in itself a massive risk signal.

If you have encountered similar "regulatory arbitrage" or "under-the-table operations" during your trading, please keep all evidence (including hidden contract clauses and email records). BrokersView encourages every victim to step forward and submit a complaint.

Hottest

Copyright © 2026 FastBull Ltd

Risk Warning

FX trading is of high risk and may not be suitable for all investors. Leverage will create additional risks and loss. Before trading, please carefully consider your investment objectives, experience level and risk tolerance. You may lose part or all of your initial investment; do not invest money that you cannot afford. Educate yourself about the risks associated with FX trading. If you have any questions, please consult an independent financial or tax advisor. Any data and information are provided "as is" and only for information purpose, not for trading or recommendations. Past performance does not predict future results.

Disclaimer

The data contained in this website may not be real-time and accurate. The data and prices on this site are not necessarily provided by the market or exchange, but may be provided by market makers, so prices may be inaccurate and differ from actual market prices. Namely, this price is indicative price only to reflect market trend, and is unfavorable for trading purpose. The provider of the data contained in the Website shall not be liable for any loss incurred by you as a result of your trading activities or reliance on the information contained in the Website.