Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

...new-orders and prices-paid soaring.

After yesterday's mixed picture on Manufacturing (PMI up, ISM down), analysts expected both Services surveys this morning to show an upward bounce.

S&P Global's Services PMI disappointed but did rise from September's 54.2 to 54.8 (but that was less than expected and less than the 55.2 preliminary print)

ISM's Services PMI beat expectations, rising from 50.0 to 52.4, well above the 50.8 expectations.

And this is happening amid a rise in 'hard' data (though admittedly based on housing and marginal labor data given the vacuum since the shutdown)

Under the hood, Prices surged to their highest in three years, new orders expanded at their fastest pace in a year and employment improved (though remained below 50)...

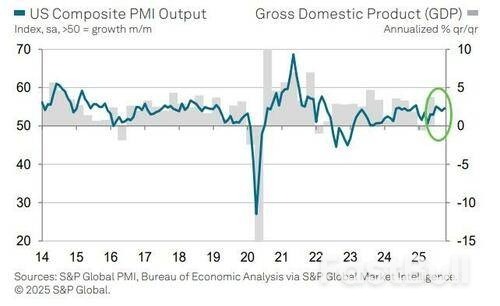

"October's final PMI data add to signs that the US economy has entered the fourth quarter with strong momentum," according to Chris Williamson, Chief Business Economist at S&P Global Market Intelligence.

"Growth in the vast services economy has picked up speed to accompany an improved performance in the manufacturing sector.

In total, business activity is growing at a rate commensurate with GDP rising at an annualized pace of around 2.5% after a similarly solid expansion was signalled for the third quarter."

While growth is being driven principally by the financial services and tech sectors, Williamson says the survey is also picking up signs of improving demand from consumers.

However, the surge in prices paid is having some consequences

"However, there are signs that new business is coming at the cost of service providers having to soak up continued high input price growth to remain competitive.

Customers are often pushing back on price rises, especially in consumer-facing markets.

While good news in terms of inflation, this lack of pricing power hints at weak underlying demand and lower profits. "

Business expectations about the year ahead have also fallen sharply and are now running at one of the lowest levels seen over the past three years, as Williamson notes "signs of spending caution from customers is accompanied by heightened political and economic uncertainty."

However, Williamson points out that lower interest rates have helped offset some of the drags to business confidence, for which the October FOMC rate cut will have likely helped further.

Certainly nothing here to shift The Fed strongly from its easing path but Treasury yields are on the rise (likely driven by the inflation jump)

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up

as of 5 November 2025. Past performance is not a reliable indicator of future performance.

as of 5 November 2025. Past performance is not a reliable indicator of future performance.

as of 5 November 2025. Past performance is not a reliable indicator of future performance.

as of 5 November 2025. Past performance is not a reliable indicator of future performance.

Fig. 1: Relative strength of US S&P 500 Financials & Technology sectors ETFs as of 4 Nov 2025

Fig. 1: Relative strength of US S&P 500 Financials & Technology sectors ETFs as of 4 Nov 2025 Fig. 2: US Wall Street 30 CFD Index minor trend as of 5 Nov 2025

Fig. 2: US Wall Street 30 CFD Index minor trend as of 5 Nov 2025