News

Analysis

7x24

Quotes

Economic Calendar

Video

Data

- Names

- Latest

- Prev

Trending Topics

To quickly learn market dynamics and follow market focuses in 15 min.

In the world of mankind, there will not be a statement without any position, nor a remark without any purpose.

Inflation, exchange rates, and the economy shape the policy decisions of central banks; the attitudes and words of central bank officials also influence the actions of market traders.

Money makes the world go round and currency is a permanent commodity. The forex market is full of surprises and expectations.

Latest Update

How to Make Forecasts with Pre-trained Machine Learning Models?

Curious about my trading success with a self-trained Decision Tree model on US stocks? Stay tuned for valuable insights and a test script of the strategy for your reference!

Full Course: Optimize Parameters for Machine Learning Model that Gives a Sharpe Ratio 5% +

Today, we delve into how to optimize machine learning model parameters to triple your invested capital and achieve an impressive Sharpe ratio of 5%+ in just 350 trades.

Full Course: Begin Mining in 10 Minutes

Think you need a super-powered computer to mine crypto? Not at all! Your trusty home computer can do the job just fine. I'll show you how to start mining from the comfort of your own home.

Full Course: How to Auto-Generate Triangle Patterns

Triangle patterns serve as crucial reference signals within the realm of trading, and today I am thrilled to unveil a remarkably efficient tool that expedites the detection of trading signals.

View All

No data

Latest Update

How to Make Forecasts with Pre-trained Machine Learning Models?

Curious about my trading success with a self-trained Decision Tree model on US stocks? Stay tuned for valuable insights and a test script of the strategy for your reference!

Full Course: Optimize Parameters for Machine Learning Model that Gives a Sharpe Ratio 5% +

Today, we delve into how to optimize machine learning model parameters to triple your invested capital and achieve an impressive Sharpe ratio of 5%+ in just 350 trades.

Full Course: Begin Mining in 10 Minutes

Think you need a super-powered computer to mine crypto? Not at all! Your trusty home computer can do the job just fine. I'll show you how to start mining from the comfort of your own home.

Full Course: How to Auto-Generate Triangle Patterns

Triangle patterns serve as crucial reference signals within the realm of trading, and today I am thrilled to unveil a remarkably efficient tool that expedites the detection of trading signals.

Early last week, gold price have soared as inflation indicators continued to rise and became more general. This, in turn, forces traders to price in more expectations of rate hikes , even if the central bank against raising rates. Despite higher treasury yields and a stronger dollar, gold remains popular as inflation-adjusted yields remain low. Gold may continue to gain support if policy makers continue to stick to a provisional route. In addition, the dot plot for next month's FOMC meeting is probably the biggest highlight of the rate hike expectations.

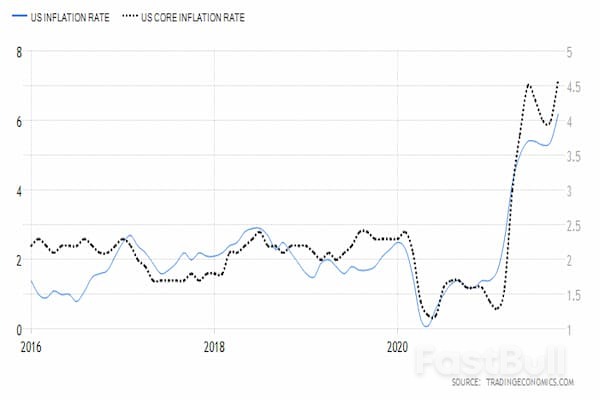

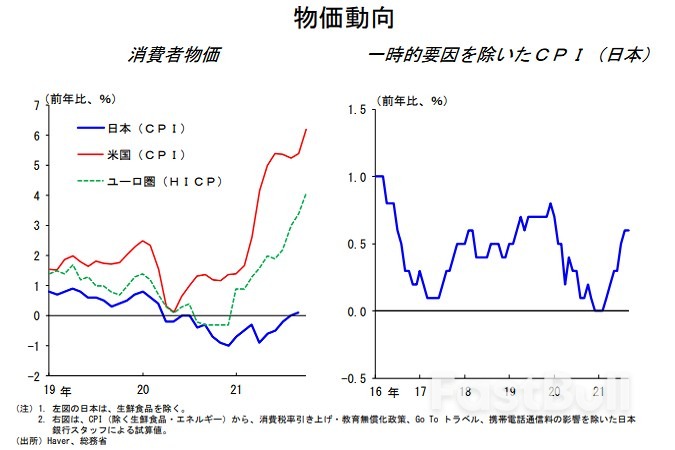

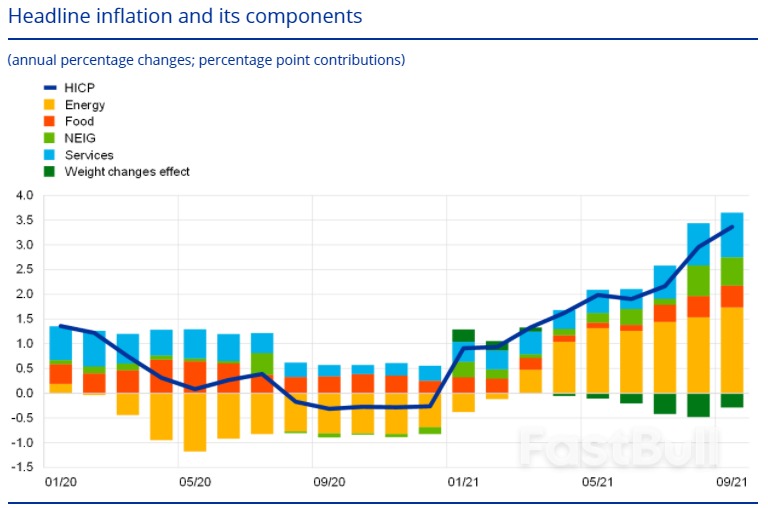

Last week, market participants may have been surprised by the October inflation rate released by the U.S. Department of Labor, as it was much higher than the market had expected. Nevertheless, the market has seen a sharp rise in prices this year, with energy and food costs, in particular, pushing the consumer price index jumping 0.9% from the previous month, well above the market forecast of 0.6%. More worryingly, The consumer price index surged 6.2% from a year ago in last month. This is the first time since November 1990 that Americans have seen inflation spiral out of control.

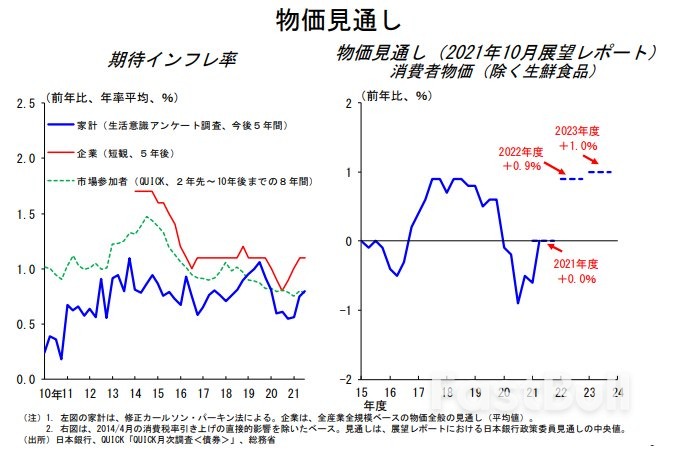

The Federal Reserve, as well as the current administration, continues to believe that the current inflation spike is temporary and will decline over time. Despite the Fed has acknowledged that current inflation is much higher than expected and will last much longer than originally anticipated. They have been emphasizing the fact that "Supply bottlenecks and labor shortages contributed to most of the inflationary pressure. " as a result of the economic recovery that has led to extremely pent-up demand. The Federal Reserve and the current administration have also emphasized that inflationary pressures will return to normal by mid-2022. However, many analysts, including myself, are convinced that the recent rise in inflationary pressures will last much longer than the Fed's forecast.

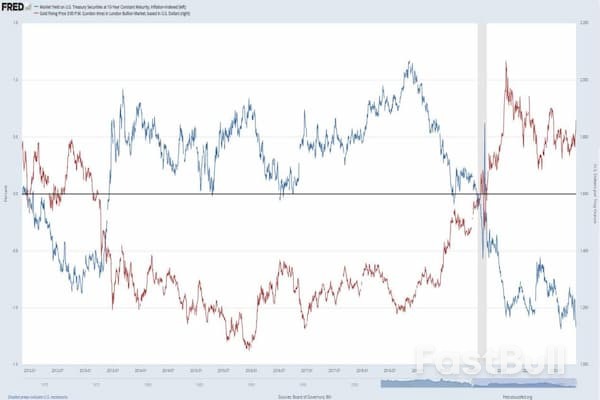

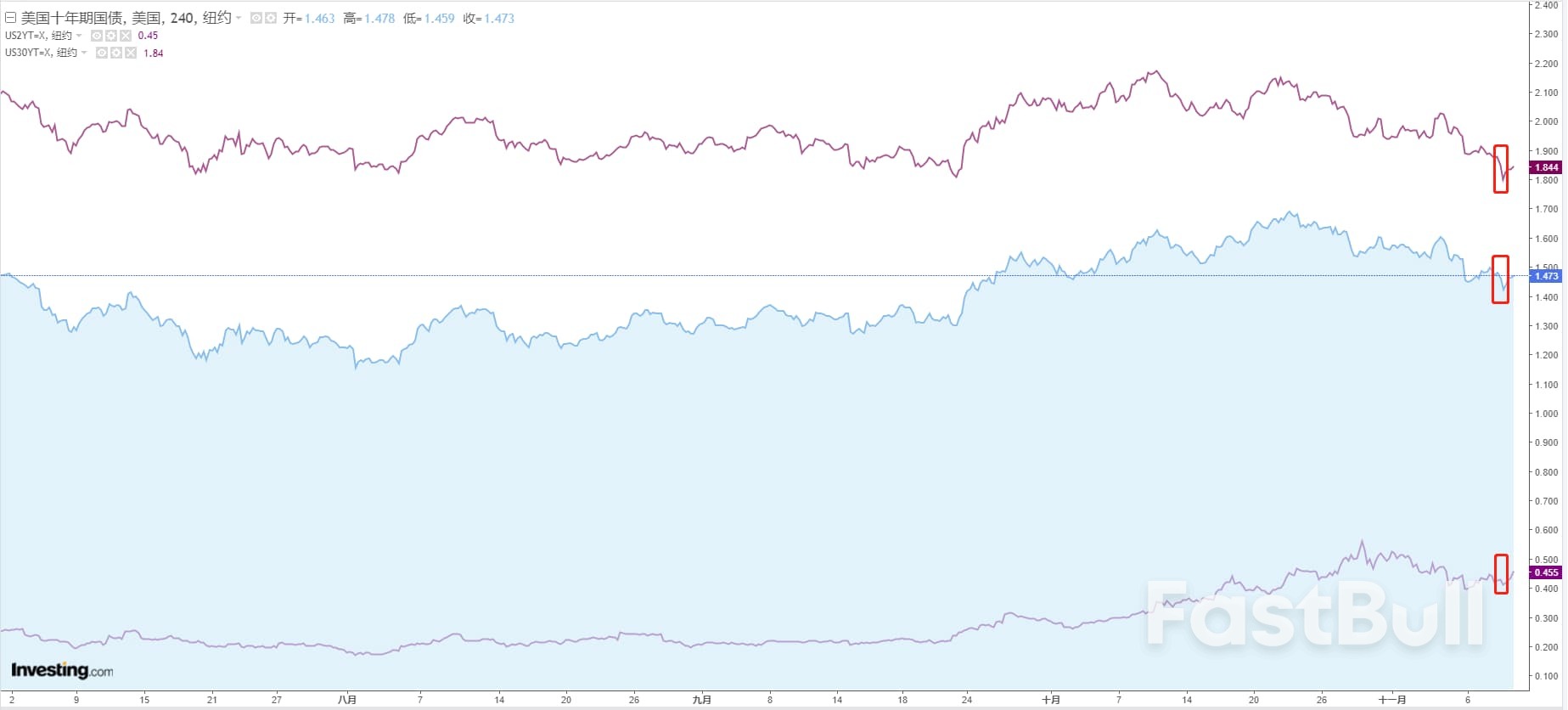

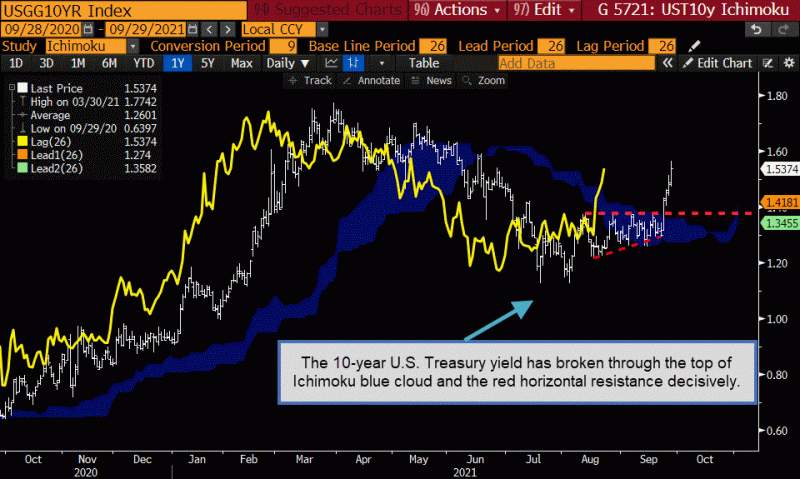

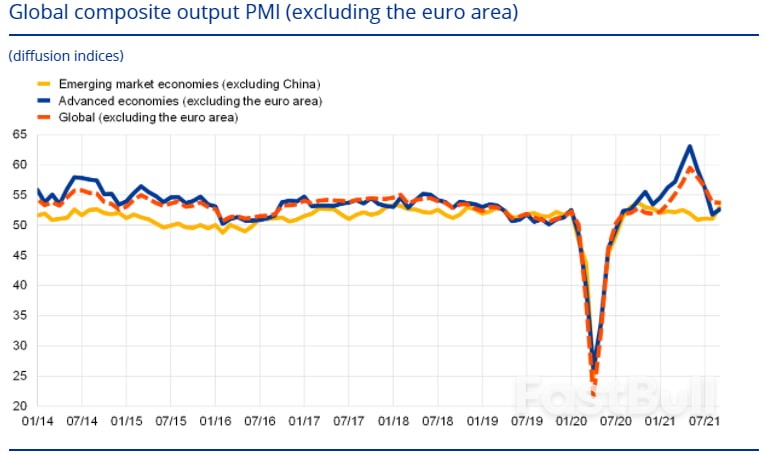

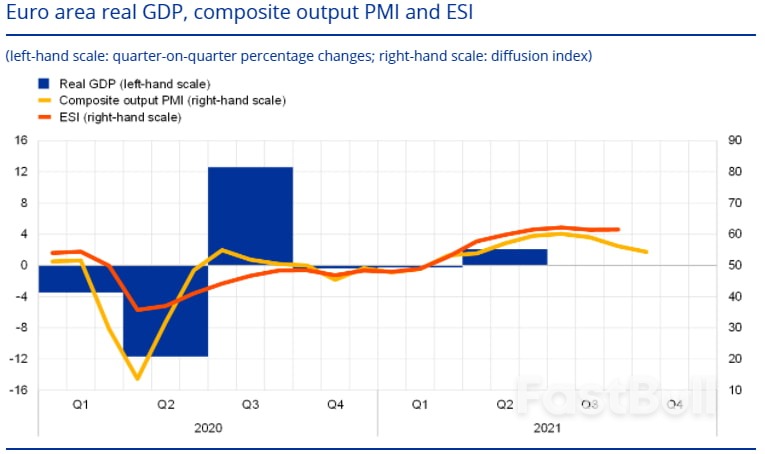

While the Federal Reserve assures that inflation is temporary, market expectations suggest otherwise. Global anxiety about inflation is mounting among businesses as the cost of raw materials rises, increasing their pressure to raise consumer prices. Despite the Fed's assurances, the 10-year U.S. Treasury yield broke through the key resistance level. Rising price pressures have accelerated inflows into inflation-protected exchange-traded funds this year. The close relationship between inflation and commodities suggests that there is more room for raw material prices to rise in the future.

In financial markets, gold prices hit a five-month record high last Wednesday, leading precious metals prices higher as data showed U.S. consumer prices surged last month, making gold more attractive as an inflation hedge.

The dollar's rally also looked quite strong throughout most of the trading day, which usually dampens demand for gold from holders of other currencies. However, the dollar eventually eased most of its gains as it touched its highest point in over a year.

Gold, as a safe haven, rose for a fifth straight day, also supported by a decline in real yields on U.S. Treasuries and overall safe-haven sentiment that pushed down major Wall Street indices.

The Commitment of Traders (COT) Reports

As inflationary pressures have increased, historically, there has been a strong correlation between inflation and commodity prices. For example, the commodity return index has a strong positive correlation with the U.S. Consumer Price Index. The regression model shows an r*square of 0.7 over the last 40 years. A positive reading of 1 implies that security prices are in step.

There was no new data from the CFTC this week, but SPDR statistics show no change in positions so far, as ETF reserves have not yet reflected any rally. This is common, as physical reserves are inert and take time to react to changes in market sentiment.

Recent research on gold's short-term and medium-term price targets has concluded that gold will trade as high as $1,835 by the end of 2021. While we agreed to think that it was reasonable for gold prices to be so high this year, we thought the time to achieve this goal was accelerating considerably when inflation for October was released last week. The latest research predicts that the gold price will test $1,900 per ounce by the first quarter of 2022.

Variables for Future Gold Prices

For the change in gold prices in 2022, we believe gold prices will be slightly below the record high in August 2020 at $2,088 per ounce. However, this study suggests that we could see gold prices as high as $2,170 per ounce. Our highest forecast would be $2,300 per ounce.

The anticipation in this study is whether inflationary pressures are really back in line with the Fed's 2% target. The Fed's target is based on the core PCE index, which was 4.4% in September. As the U.S. core PCE ignores rising food and energy costs, the market generally believes it is unrealistic to use the indicator in this inflationary environment. Energy and food costs are the biggest factors contributing to the CPI's recent inflation rate of 6.2%. Based on the CPI inflation index, we believe that near-term inflationary pressures will remain at record highs for most of 2022 is more realistic.

The risk of loss in trading financial assets such as stocks, FX, commodities, futures, bonds, ETFs or crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No consideration to invest should be made without thoroughly conduct your own due diligence, or consult with your financial advisors. Our web content might not suit you, since we have not known your financial condition and investment needs. It is possible that our financial information might have latency or contains inaccuracy, so you should be fully responsible for any of your transactions and investment decisions. The company will not be responsible for your capital lost.

Without getting the permission from the website, you are not allow to copy the website graphics, texts, or trade marks. Intellectual property rights in the content or data incorporated into this website belongs to its providers and exchange merchants.

At the plenary session of the House of Representatives on the 10th, Hiroyuki Hosoda, the chairman of the largest intraparty faction of the LDP, the Seiwa political research council, was elected as one of the speakers of the House of Representatives. As a rule, the speaker will leave the party membership. For this reason, senior officials of the

At the plenary session of the House of Representatives on the 10th, Hiroyuki Hosoda, the chairman of the largest intraparty faction of the LDP, the Seiwa political research council, was elected as one of the speakers of the House of Representatives. As a rule, the speaker will leave the party membership. For this reason, senior officials of the