Markets

News

Analysis

User

24/7

Economic Calendar

Education

Data

- Names

- Latest

- Prev

This move, across the PM complex, has been driven by largely by three factors – increased demand from central banks (especially in EM) seeking to diversify their reserve holdings.

This move, across the PM complex, has been driven by largely by three factors – increased demand from central banks (especially in EM) seeking to diversify their reserve holdings; investor worries about the inflation outlook, chiefly the risk of higher inflation becoming embedded; and, the unsustainable fiscal path on which most DM economies continue, with government spending, frankly, out of control.

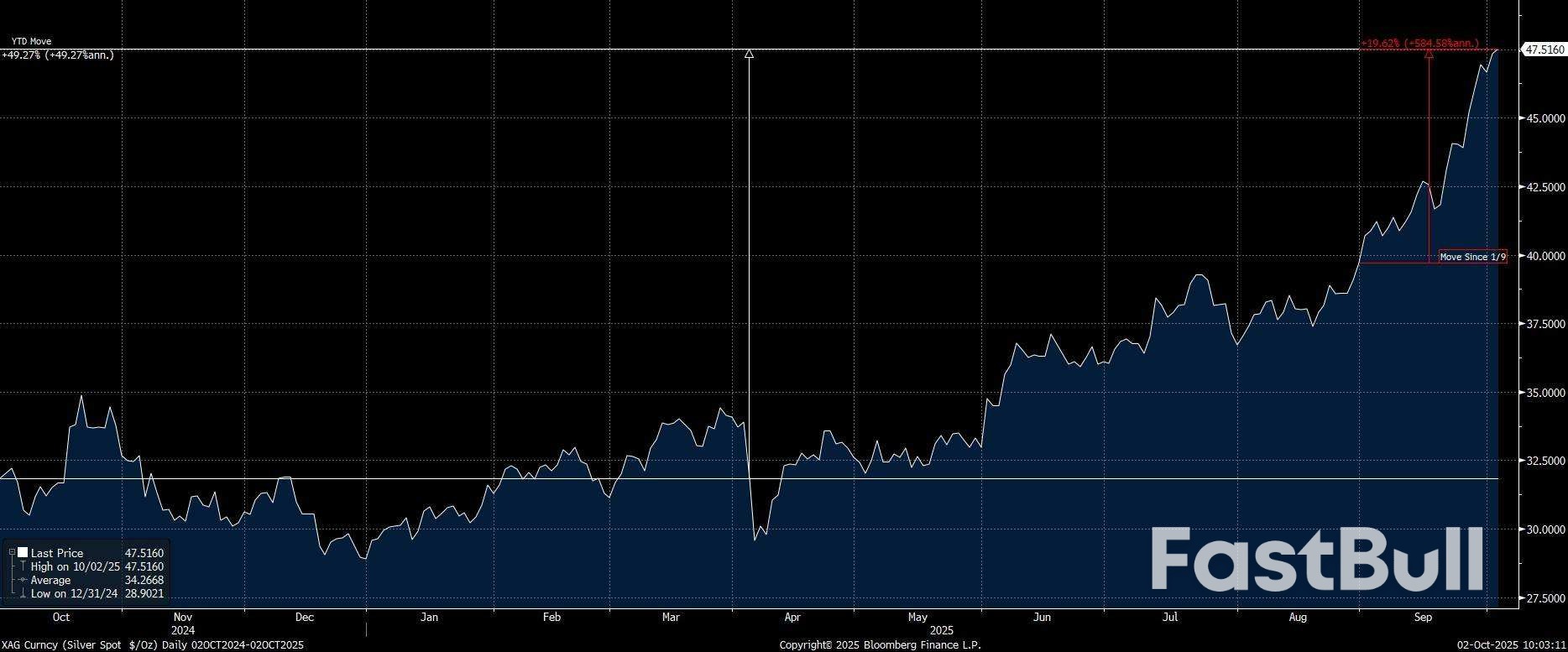

Perhaps one of the most interesting things about the recent rally is the way in which silver has been trading almost tick-for-tick with gold. This is somewhat unusual given how silver is typically much more risk-sensitive than its golden cousin, and suggests that physical demand (aka hoarding) for precious metals is one of the biggest drivers of upside right now.

On that note, while the rally has come a very long way this year, there are several indications that the move has more room to run. In terms of physical demand, in particular, while holdings of silver in ETFs have risen substantially in 2025, they are still some considerable way ff the highs seen in early-2021, again suggesting potential for further upward pressure on price if demand continues to increase.

From a fundamental perspective, there is little which leads me to believe that any of the three main drivers of the rally mentioned earlier are likely to shift substantially any time soon. EM reserve allocators are likely to increasingly diversify reserves, especially as President Trump's ‘America First' policies continue; the risk of inflation expectations becoming un-anchored continues to linger, especially as the Fed cut rates and embark on a ‘run it hot' strategy; while, government spending shows no sign of slowing any time soon, chiefly in the US, where the deficit already stands at roughly 7% of GDP, a level only previously seen during recessions.

That said, no asset tends to go up in a straight line forever, and in many ways pullbacks within a longer-run rally are a healthy and normal part of market functioning, which actually result in a more durable overall trend.

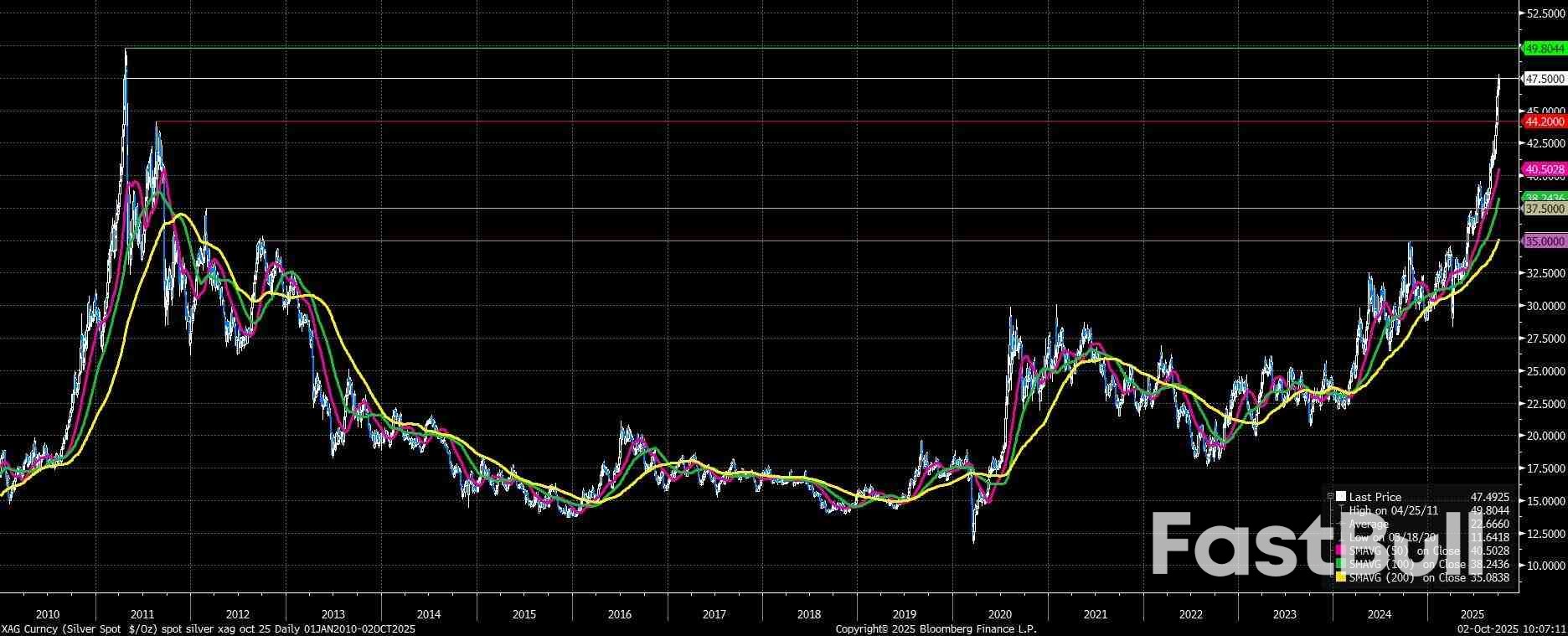

Right now, spot silver is running into a little resistance around $47.50/oz, which coincides with the levels seen in 2011, just prior to the spike to record highs seen in April of that year. If the market is able to convincingly clear this level, then a move back to those record highs, and probably north of $50/oz for the first time, seems almost a given. Taking into account the distinct lack of any notable levels between these two points, such a move, were it to occur, could be explosive and rapid in nature.

To the downside, given the rapid nature of the recent rally, notable support doesn't really emerge until the 50-day moving average at $40.50/oz, beneath which the 2012 highs at $37.50/oz lurk. Prior to this recent bull trend, $35/oz had been a ‘cap' on price for some time, and obviously is a notable level as a result, though my view is that a test of that level seems a very long shot indeed at this moment in time.

Overall, then, the fundamental bull case for silver continues to hold water, while momentum clearly remains with the bulls for the time being. To lean on an old market adage, ‘the trend is your friend' very much seems to apply here, with further upside likely on the cards short-term, and any dips representing medium-term buying opportunities.

728 RM B 7/F GEE LOK IND BLDG NO 34 HUNG TO RD KWUN TONG KLN HONG KONG

The risk of loss in trading financial instruments such as stocks, FX, commodities, futures, bonds, ETFs and crypto can be substantial. You may sustain a total loss of the funds that you deposit with your broker. Therefore, you should carefully consider whether such trading is suitable for you in light of your circumstances and financial resources.

No decision to invest should be made without thoroughly conducting due diligence by yourself or consulting with your financial advisors. Our web content might not suit you since we don't know your financial conditions and investment needs. Our financial information might have latency or contain inaccuracy, so you should be fully responsible for any of your trading and investment decisions. The company will not be responsible for your capital loss.

Without getting permission from the website, you are not allowed to copy the website's graphics, texts, or trademarks. Intellectual property rights in the content or data incorporated into this website belong to its providers and exchange merchants.

Not Logged In

Log in to access more features

FastBull Membership

Not yet

Purchase

Log In

Sign Up